A balanced scorecard (BSC) is a management framework or technique used by businesses to measure performance and obtain feedback on ongoing strategies that work towards the business’s objectives and vision.

It is fundamentally a performance metric that keeps track of internal business components of a strategy such as strategic objectives, targets, measures, and initiatives, which can be improved and controlled to influence the desired outcome. This way, businesses can keep a “scorecard” and measure how an adopted strategy is performing in comparison to the expected or projected results. It considers micro-components of a business while giving a picture of the overall business position (health).

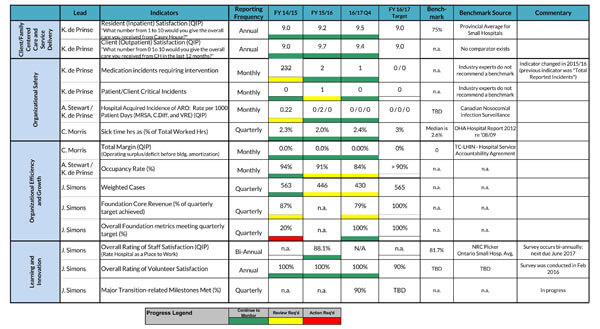

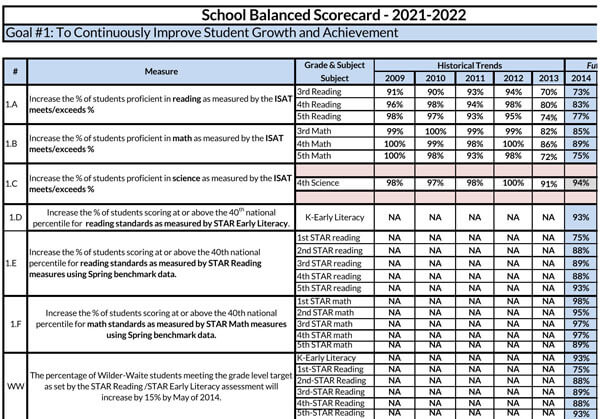

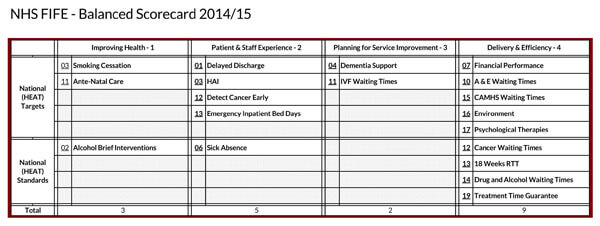

Balanced Scorecard Templates

Invention

The BSC technique was first published in 1992 by Dr. Robert Kaplan and David Norton. To develop the framework, they incorporated non-financial information in the previously used metric performance measures. As a book, BSC was published in 1996. Though initially intended for for-profit organizations, it was later adapted to fit non-profit organizations and government agencies due to its popularization by the paper and the book.

Even though Art Schneiderman is believed to be the creator of the balanced scorecard, Norton and Kaplan are the recorded first publishers of the framework as Schneiderman referenced them in his work.

Basics

The introduction of non-financial metrics created “balance” in the measurement of performance of business strategies that were lacking in the previous performance frameworks that focused on financial measures. The fact is there are other factors other than growth and profitability that influence the health of a business or organization. To factor in these components, the BSC looks at four “perspectives” of an organization; financial, customer, internal processes, and organizational capacity.

More than a “scorecard”, BSC is a methodology that identifies specific financial and non-financial objectives, sets targets to be achieved, and identifies key strategic projects (initiatives) that align with the organization’s vision. This way, BSC as a methodology helps set strategic objectives and identify specific initiatives that drive the objectives, and provide a way to measure the outcomes (objectives).

Where is It Used?

A balanced scorecard can be used by organizations to assess different areas of an organization. It can be applied in the following sections of an organization:

- At the corporate level, strategy implementation

- Information Technology strategies

- Post-merger strategies

- Joint venture and alliances strategies

- In reward alignment and HR strategy

- Merging departments strategy with corporate strategy

- Budgeting and resources allocation

- Managing initiatives

Four Perspectives

The health equation of an organization is dependent on different functions which play distinct but equally significant supplementary roles. Therefore, companies and organizations must put all of them into considerations when implementing strategies.

These different aspects can be broadly categorized into the following perspectives:

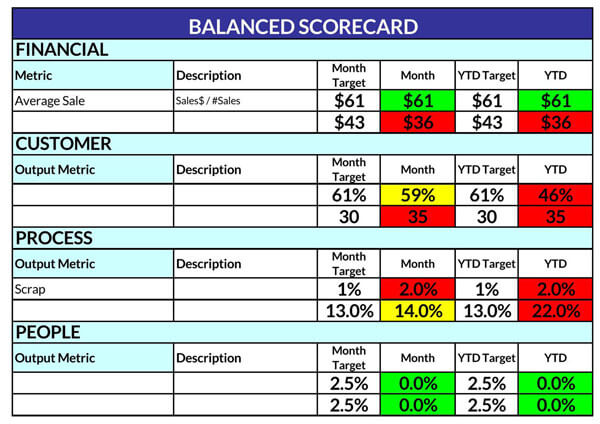

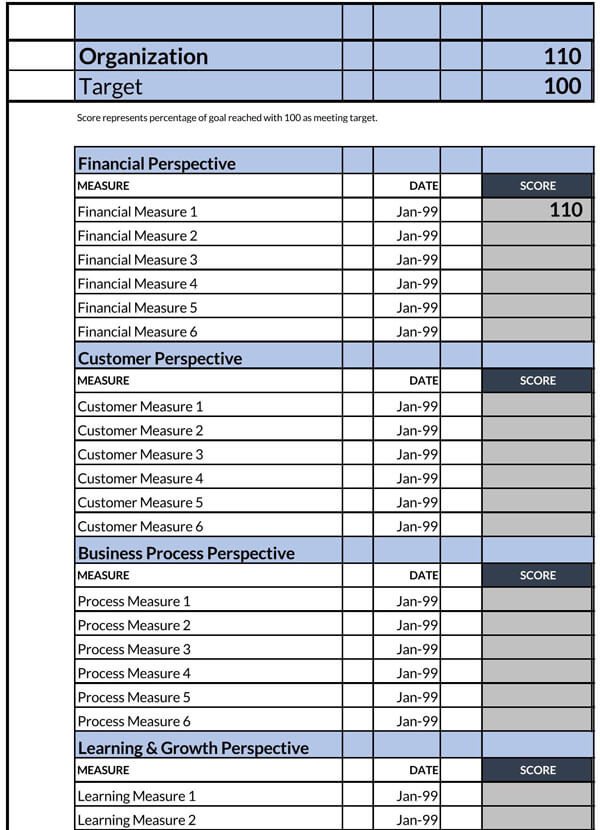

Financial

The first perspective is financial that addresses the financial figures that demonstrate the performance of an organization. Financial position is mandatory for an organization to thrive. The financial perspective investigates aspects such as revenue (sales), profit, operating costs, asset turnover, liquidity, expenditures, and ratios such as return-on-equity (ROE). It is what the shareholders see and what attracts investors. Financial performance is the easiest to define and measure. Financial metrics include dollar amounts, income targets, financial ratios, and budget variances.

Customer perspective

The balanced scorecard also investigates how the customers perceive the organization. The customer’s perspective is important in enhancing sustainability. The aspect used to define and measure customer perspective is customer satisfaction. Customer satisfaction can be measured in terms of quality, timelines, performance, service, and cost (pricing). The organizations should be able to offer what the customers need from it.

Internal Processes delivery

The internal processes perspective examines how well the business is being operated and the quality and efficiency of product manufacture and service delivery to customers. The objective is usually optimization – obtaining the best results with the available resources.

Organizational capacity

Organizational capacity observes the employees, information, management/leadership, infrastructure, and technology. The BSC outlines how to create value in these aspects through improvement, learning, and innovation and concert this to a competitive advantage.

Components of BSC

The components of a balanced scorecard are interrelated and do not operate independently when it comes to strategic implementation. They are combined to achieve the organization’s goals and objectives.

Each perspective is examined in a BSC through the following components:

Objectives

The BSC should have general organizational objectives such as profitability, customer satisfaction, or market share that can be broken down into strategic objectives. The objectives are characterized as follows:

Applies to all-level organizations

The objectives should impact and be impacted by all the levels of the organization. Typically, there are multiple departments (levels) in an organization; the objectives should be inclusive of the contribution of each department (level).

Don’t explain the project but the objective

When defining the objectives, the expected outcome should be the core of the objective, not the process or project of attaining the outcome. Each objective should be specific too.

EXAMPLE

The project could be “Invest $100 000 in marketing and advertising”, but the strategic objective would be “To increase market share by 10%.”

The outcome demonstrates performance improvement

Each objective should be Specific, measurable, achievable, realistic, and time-specific (SMART), meaning the outcomes (objectives) of the strategy ought to be measurable to measure performance and improvement. Remember, projects and initiatives and, consequently, strategic objectives are merely steps towards a predetermined end-goal; measurement of performance is thus important in remaining on track towards the goal(s).

Measures/KPIs

It ought to outline performance measures or Key Performance Indicators that the organization uses to keep track of the progress made towards the strategic objectives. Strong KPIs should be adequate to determine if a strategy is feasible and easily understood by all the stakeholders. Each objective should be assigned at most three KPIs.

Note that KPIs are not the desired outcome but rather things that can be used to measure accomplishments, indicate the success of a project or activity, and shows changes in outcomes over time. Also, KPIs reduce the uncertainty associated with waiting until the termination date of a strategy to determine if it works.

KPIs can be used in the following aspects:

Organization’s health

KPIs can be used to determine the organization’s health. The measures must clearly illustrate the progress made in achieving the strategic objectives and must be interpretable to indicate how the strategy influences the organization’s position towards achieving its goals.

Focus

KPIs help in shrinking the outcomes of different strategic activities into a small number of outcomes that were influenced by those activities. This way, the company or organization can focus on the changes of a small number of outcomes when measuring the progress of the strategy instead of measuring the outcome of each activity. KPIs ought to have leading (input or predictive) and lagging (output) measures.

However, lagging measures such as profit and expenses are commonly focused on in strategic plans, for they are accurate and easy to measure. Leading measures such as the number of units produced or average hours of workers, on the other hand, despite being difficult to identify, are easier to influence to accomplish goals.

Initiatives

Initiatives should also be presented in the BSC. Initiatives are the different actions the organization will take to meet its strategic objectives. Initiatives and projects answer the “How” question and represent how the set objectives are achievable. Ordinarily, each initiative will have a beginning and end date catering to the “realistic and time-specific” characteristic of strategic objectives.

Target

Finally, the BSC should have targets associated with the strategy. Targets can be organizational and/or department-wise targets that are projected to help the organization realize the measures set.

note

Balanced scorecards should be crafted to reflect the diversity or uniqueness of the organization using them.

Some of the different ways to do this are by personalizing it to reflect the organization’s target audience and brand and including the company or organization details such as a logo.

When to Fill a Strategy Map

A strategy map is a management tool or model that presents a company’s or organization’s strategic plan visually on a single sheet of paper. It shows all the components of the plan and how they relate to each other. A strategy map should be designed before the completion of the BSC. The most recommended time is after setting the objectives but before identifying the measures.

The four perspectives that appear on a scorecard should also appear on a strategy map. The strategy map shows the direction of progress – how one activity and/or a group of initiatives lead to the desired outcome.

Methodology of a Balanced Scorecard

The creation and utilization of a scorecard in a company or organization can be achieved in a few steps. They include:

- Conduct a detailed internal assessment of the company or organization

- Identify existing and potential challenges facing the organization

- Get input from stakeholders (management, employees) by hold in-person meetings

- Consult with management to get the go-ahead and finalize high-level objectives

- Through consultations, assign strategic objectives to management teams and define measures

- Set initiatives

- Involve management and set targets for each measure of the strategy.

Key Benefits

The BSC approach is widely used by organizations due to its dependability when measuring the performance of strategic plans.

Some of the common significances of a BSC are:

Better strategic planning

It offers a systematic approach to coming up with strategic plans. By establishing the relationship between the four components (objectives, measures, initiatives, and targets), the organization can clearly see how they will move from point A to point Z of a strategic plan. Using leading and lagging measures, an organization can set goals and determine actual success and advancement towards these goals, thus avoiding strategies that have no benefits or positive impact on the organization.

Improved performance reporting overall

It is an effective communication tool in management. A BSC ensures that objective reporting is exercised in an organization as each team or department already clearly understands the strategic objective and measure (management expectations) required from them. Consequently, unnecessary reporting is avoided.

Facilitates the budgeting and resource allocation process

By assessing the financial, customer perspective, internal processes, and organizational capacity perspectives, a company or organization can use a BSC to prioritize when distributing funding and resources. They can identify areas that need additional funding to achieve the organization’s goals.

Efficient tracking of strategy implementation

Companies and organizations use KPIs to track the implementation of strategic plans. By allocating deadlines and milestones to initiatives, a company or organization can implement a strategy in phases which reduces ambiguity associated with one strategy implemented over a long period.

Keeps management focused and clarify roles of different teams

It is a one-stop-shop of an organization’s strategic objectives and what needs to be done. This way, all involved participants can remain focused on what the company or organization intends to achieve with a specified strategy. When outlining actions plans and projects involved in a strategy, a BSC identifies parties responsible and their respective roles, thus eliminating confusion during the execution process.

Frequently Asked Questions

A strategy map is a visual interpretation of a strategy through images, shapes, graphs, text, gauges, and numbers, whereas a BSC is a framework for creating and measuring the performance of the strategy. A strategy map indicates the cause-effect relationships between strategic objectives, while a BSC is more comprehensive for other than strategic objectives; it outlines Key Performance Indicators, initiatives, and target measures.

The period which it takes to prepare a BSC will vary from one organization to another. However, ordinarily, it will take 8 weeks to develop a corporate scorecard which is prepared in two phases. The first phase involves preparing the strategy map, which takes about 6 weeks to finalize, and the second phase, which involves the preparation of a BSC that takes 2 weeks to finalize. If an organization has 6-8 departments, this process will typically take 10 – 12 weeks. A two-phase approach is also involved, each for corporate and individual departments separately.

About This Article