An Estate Planning Checklist is an official document used as a manual of how individuals can plan their assets or property and end-of-life wishes to be handled should they become incapacitated or pass on.

By referring to this checklist, individuals expecting to use it can get a general understanding of estate laws applicable in their State. This way, they can choose a planning checklist that best suits their financial and health care needs. By selecting a befitting checklist form, individuals can choose a person best suited to carry out their wishes in terms of personal finances and end-of-life health care requests in the event they are unable to execute them themselves. This checklist allows the user to predetermine the beneficiaries of their estate or if they would like to subject it to the probate process.

Free Templates

Related Forms

The utilization of other related documents supports the execution of this checklist. These documents have specific functions but work together towards a holistic intention.

They include:

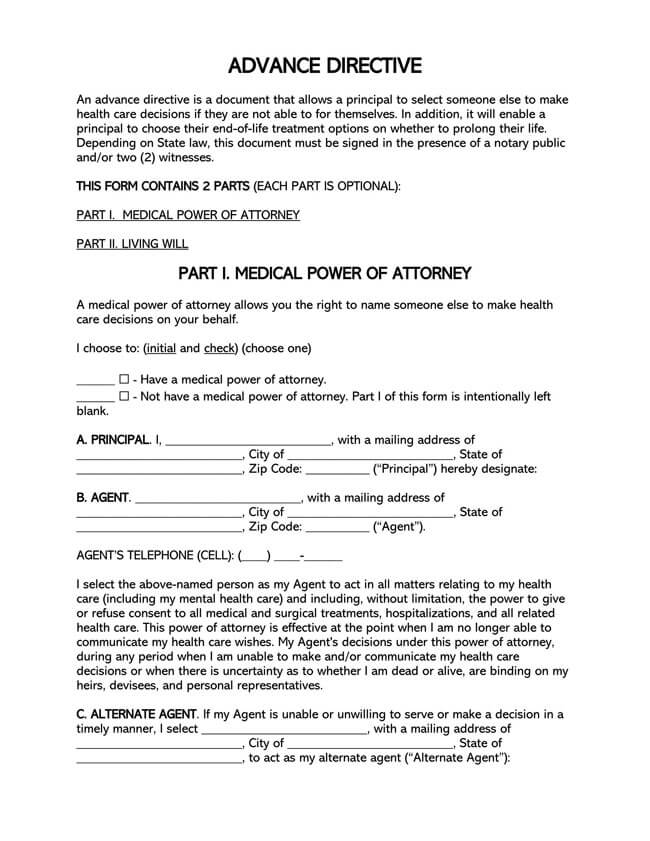

- Advanced directive – This document allows a person to choose another person (agent) to make decisions on medical /health care matters should a situation arise where they cannot make the decisions themselves. An individual can also outline their preferred end-of-life treatment options through an advanced directive, allowing them to plan such an event and avoid medical procedures they would not like to be subjected to.

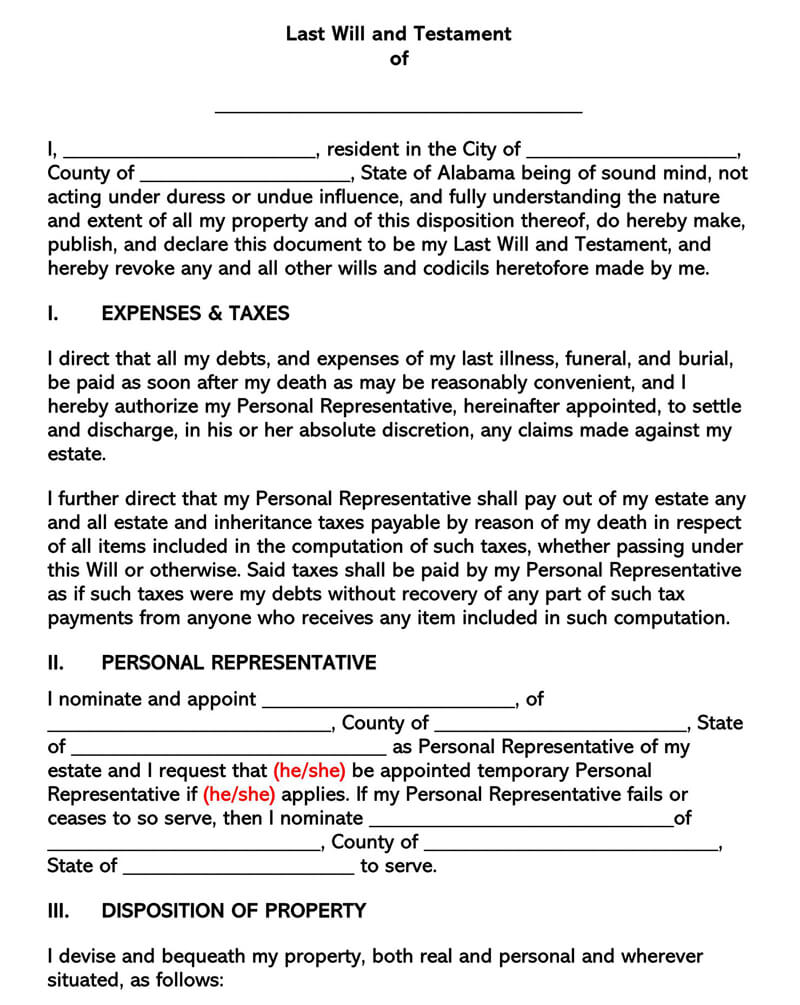

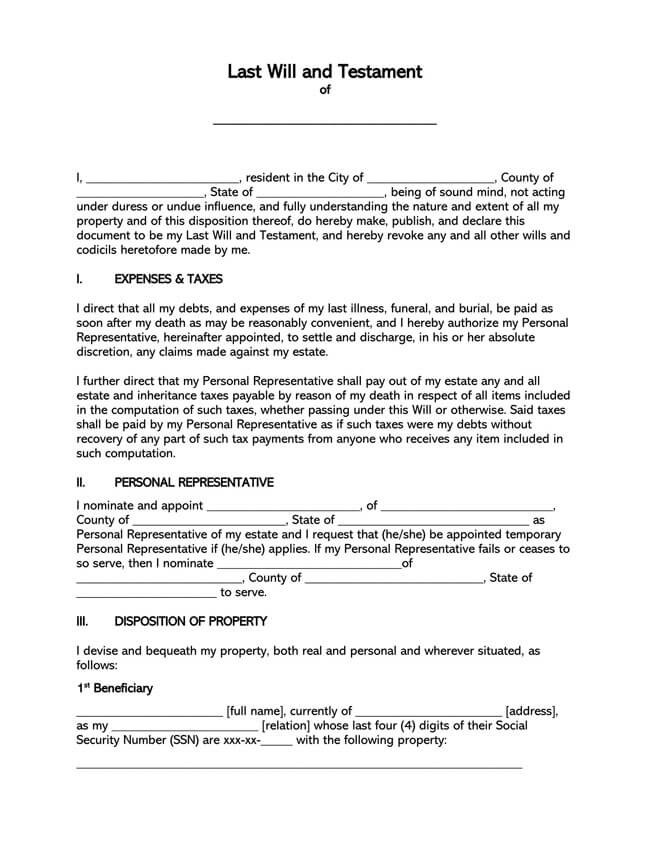

- Last will and testament – Also known as the last will, directs how personal assets or property should be distributed to a person’s heirs or beneficiaries, commonly spouses or family members. The last will helps an individual to distribute assets to people who rightfully deserve them and avoid a lengthy probate process and disputes during their distribution after death.

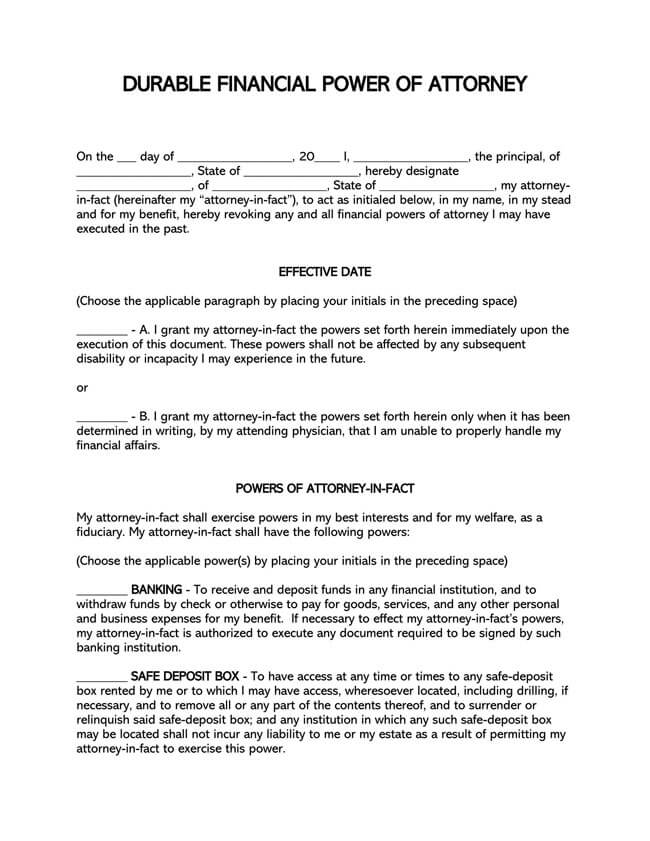

- Power of attorney – A POA is used to appoint a person responsible for making financial decisions on behalf of the appointing party when they are still alive but unable to attend to the matters outlined. Financial decisions will often be related to a person’s estate and hence the importance of a POA when planning using this checklist, especially when a person is incapacitated.

Creating an Estate Planning Checklist

This checklist should be compliant with state laws, and as a result, one should first acquaint themselves with applicable estate laws in their State. Once this is done, the writing process can commence.

The steps provided below can be adopted for this process to obtain a well-organized and effective planning checklist for estate:

Select a medical agent

First and foremost, most estate planning advisors recommend that individuals begin with their medical/health care requirements in the checklist.

This will customarily involve the utilization of the following documents:

- A living will – Through a living will, one can state their end-of-life wishes should they become incapacitated to a point they cannot communicate their wishes or make decisions themselves. A living will allow one to plan what medical procedures they would like to avoid, such as receiving food or fluids through IV. It is to be noted that Living wills are state-specific.

- A medical power of attorney – A medical POA permits a person to select another person to be their health care agent and grant them authority/power to make medical decisions on their behalf. This way, the estate planning checklist user would not have to worry about medical personnel acting contrary to his or her best interests if he or she cannot make the medical decisions himself or herself.

- Caregiver agreement – A caregiver agreement used when assigning a caregiver, such as a nurse who is paid to carry out daily errands and look after an older person or an individual with special needs.

When all these documents are combined, they are jointly referred to as an “Advance Directive.” The estate planning should indicate who the appointed party is if any of the pre-arrangements are to be realized.

Select a financial agent

Secondly, one should appoint a financial agent, also known as an attorney-in-fact. This can be done through a Durable Power of Attorney. The attorney-in-fact is tasked with making decisions on matters finances on behalf of another party. The agent should be identified by name, address, and contact information in the checklist. They do not have to be legal counsel (attorney); however, it is highly recommended that someone trustworthy should be selected.

The powers that can be transferred through a Durable POA if directed by the principal include;

- Management of Real Estate

- Management and distribution of Personal Property

- Trading of Stocks and Bonds

- Handling of possession or Commodities owned by the principal

- Gifts

- Carry out set out activities and operations of business entities

- Collect and apply for insurance

- Develop and set in motion retirement Plans

- File for personal or corporate taxes (State and Federal)

It is advised that the same agent handling finances should be the one to handle health care/medical responsibilities.

Create a list of assets

Thirdly, this planning checklist should have a list of all the assets under the current owner. They are all the assets and property that jointly make up the “estate.” This step is essential to have an idea of the estate’s total value (net worth). The list should outline any personal assets, real estate property, investments, vehicles, business entities, valuable possessions (such as art and jewellery), and any other possessions together with their estimated value. Any life insurance policies owned by the person should also be included.

Determine the beneficiaries

After listing the assets, the planning checklist for an estate should outline who are the beneficiaries/heirs of the estate. Beneficiaries are individuals to whom the estate will be transferred if the person dies. Ordinarily, the beneficiaries of a person are; the spouse if he or she is married and their children, if any. The checklist should identify the beneficiaries by the legal and official names. The selection of beneficiaries is solely at the discretion of the property owner. Beneficiaries can also be companies, organizations such as foundations, and non-profit organizations, not just people.

Decide a trust or a will

The next step should be to provide documents necessary for the legal transfer of the estate to the heirs/beneficiaries.

Transfer of ownership can be done through:

- Last will and testament – Commonly termed as a “Will.” It is meant to indicate by name who will get what upon the death of a property owner. The distribution of property will sometimes have to be through a probate process that lasts anywhere from six months to twelve months.

- Living trust – Used by individuals who wish to avoid the probate process by allowing the initiator of the living trust to be the trustee and continue collecting money being generated by the living trust’s assets or property. A living trust is recommended as the beneficiaries get to elude the tedious probate process. It is also hard for other family members to question the authenticity of a living trust.

Whichever means an individual opts to use; the document should be attached to illustrate who was mentioned in the will or trust clearly.

Sign the documents

Subsequently, the planning checklist for estate should be signed to validate it. The document’s signing should be done according to the State’s signing requirements (execution laws). Typically, this will involve having two witnesses and a notary public approve it. It is recommended that the witness should not be beneficiaries or agents in the estate documents. The names, signatures, and date of signing should be provided.

This checklist can be notarized at different places, including available online platforms; financial institutions such as Bank of America provided one has an account with them, UPS Store, and National Association of Notaries.

Keep in a safe place

The final step is to keep the original document in a safe place, such as a personal safe or with the one’s attorney, where it can be accessed for reference if need be. Copies should be handed to trusted family members and friends.

Conclusion

For individuals wondering how to plan the handling of their assets and end-of-life needs once they become incapacitated or pass on, an estate planning checklist is an effective way of going about it. State estate laws are used to govern the writing of this checklist. Ordinarily, this checklist will outline how one wishes their medical, financial, and transfer of assets to be handled. This involves selecting a medical agent, which is done through a living will, medical power of attorney, or a caregiver agreement. Finances are addressed through a Durable power of attorney. Transfer of assets is addressed by making a list of assets, selecting the beneficiaries, and indicating if a trust or will is used. Estate planning should be witnessed and notarized.

About This Article