The asset purchase deal occurs when a buyer agrees to purchase specific business assets as mentioned in the agreement. This agreement will detail the whole deal’s structure, including the warranties, limitations, and price. This is a document that tends to have massive financial and legal implications for both parties.

But generally, we need to know what an asset purchase agreement is.

The Asset Purchase Agreement (APA), or business purchase agreement, is a legal written document that sets out the terms and conditions for purchasing and selling a significant business asset or the business itself.

The APA, however, unlike a stock purchase agreement, doesn’t include the business’s liabilities. The company retains any liabilities that the buyer doesn’t want to assume in the asset purchase deal. At the same time, all parties involved need to ensure the asset sale is being made at a fair market value. Also, all parties involved should ascertain that the company can sufficiently pay any debts and liabilities that have not yet been assumed. Otherwise, if this is not considered, the deal may be deemed fraudulent.

note

For the above-mentioned reason, it would be advisable that you get a corporate lawyer to assist you with negotiating it and drafting a vital document. That ensures your asset purchase agreement is enforceable and fair under the law.

Free Asset Purchase Agreement Templates

Types of Asset Purchases

An asset purchase includes either intangible or tangible assets. In most cases, buyers opt for asset purchases as they can easily buy what matches their needs as well as the kind of liabilities they would comfortably assume. If there are certain pieces of the business that the buyer doesn’t want, they can always be carved out before the agreement is finalized.

The asset purchases include, but are not limited to:

- Machinery

- Licenses

- Property and Premises

- Stock

- Equipment

- Intellectual property

- Businesses

- Goodwill, among others.

Difference Between Asset Purchase and Stock Purchase

In the process of an asset purchase, a buyer often consents to buy specific assets of a business without any liabilities. This means that the buyer takes on the risks and rewards of those particular assets. Also, in an asset purchase, the capital assets are taxed as capital gains, whereas the other assets get taxed as ordinary income.

On the flip side, the buyers assume ownership of the entire entity in a stock purchase, including all its assets and liabilities. The stock purchase is even taxed as a capital gain, and the assets are not adjusted to a fair market value. Therefore, business continues as usual even after a stock purchase.

Real-World Difference in Asset Vs. Stock Purchase

In a stock purchase, a buyer purchases all the assets and liabilities of a specific company. As long as the business continues to operate with its legal owner, the purchaser gets ownership of the business. A good example is the purchase of LinkedIn by Microsoft back in 2016. Microsoft acquired LinkedIn at $196 per share and successfully fought for it against its competitor Salesforce.com.

Once the announcement was made, the value of LinkedIn shares rose by 64%. The deal was all cash, and that also included LinkedIn’s net cash. The reason for this deal was for the 433 million LinkedIn subscribers to help Microsoft boost its data productivity.

On the other hand, asset purchase occurs when a company purchases one or more assets of the target business. An excellent example was when Disney acquired 21st Century for $71.3 billion. The assets acquired by Disney included 20th Century Fox, Indian channels like Star India, Fox Searchlight Pictures, and National Geographic Partners, among others. It was an asset acquisition deal.

Benefits and Shortcomings

Before entering into an asset purchase agreement, it’s vital to weigh the pros and cons of the deal. That’s in terms of the price, the complexities of getting the deal done, as well as any future tax implications.

Naturally, most buyers will prefer asset purchases due to the security of tax advantages. However, asset purchases tend to be much more complex and require both parties to be very keen.

For this reason, there are risks a buyer may encounter in an asset purchase. Some of these pros and cons include:

Benefits

- Structure of the transaction: The asset purchase agreement has several advantages, but the main one is that the buyer can dictate what assets go into the transaction. This limits the buyer’s exposure to significant, unknown, and hidden liabilities that the seller may have failed to state.

- Assets are sold at a fair market value: Another significant advantage of APAs is that the buyer can step up the basis of many assets over their current tax values. Unlike stock purchases, the buyer can allocate their purchase price among the assets to reflect the market value. That helps the buyer obtain tax deductions for amortization and depreciation.

Shortcomings

An asset purchase comes with its fair share of complexities as compared to a stock purchase agreement. In that case, some specific assets must be wholly reassigned to the APA. In other cases, the contracts may even need to be renegotiated. Also, there is the risk of customers being spooked by the deal due to the number of complexities involved. To an extent, they may refuse to sign a contract with the buyer. You may also need to rewrite employment agreements and re-title certain assets to the buyer.

Basic Requirements of Asset Purchase Agreements

When it comes to an asset purchase agreement, you need to include all essential information and details in depth to avoid any misunderstandings. That’s because it serves multiple purposes for the benefit of all parties involved. General components in an APA can be pathways for either the seller or buyer to take advantage of the terminologies or loopholes.

The most reliable components are listed below:

Goodwill

Goodwill is a distinct asset. It is considered the amount paid for a business over its identified assets, or the fair market value. Goodwill includes assets that help the business remain competitive and attract new customers, which most newly established companies would struggle with. Goodwill consists of the company’s brand name, reputation, the business’s proprietary technology, connections with other businesses, a solid customer base, and excellent employee relations. Goodwill is included primarily in the APA as an asset category for accounting and Tax purposes and represents the synergy among the assets of a business to produce its income.

VAT

VAT should be charged on transferring each asset according to the rules that apply to each asset. That would be the zero rate, standard rate, reduced rate, or exempt. However, where a business is transferred as a going concern, additional rules override these basic principles.

If the transfer meets the conditions to be a Transfer of Going Concern, the buyer will not pay VAT for the acquisition of the assets. On the other hand, the seller must not charge VAT if a business transfer meets TOGC conditions.

However, if the business purchased any fixed assets and paid VAT on the purchase, the VAT is not counted as part of the fixed asset cost. That’s because the business can get allowances for that. Therefore, the purchase cost of the fixed assets in an asset transfer and the VAT should always be indicated separately.

Employees and TUPE

When buying the business assets of a company to continue it as a going concern, you need to consider the position of employees. Employees of the business are subject to TUPE (Transfer of Undertakings Protection of Employment Regulations 2006), which applies to protect employees in different situations.

When TUPE is applied to an asset purchase, employees of the business are automatically transferred to the new owner along with the company. According to TUPE, any changes to the employee’s contract of employment by transfer are void unless the employee consents. Regarding the transfer, there are statutory requirements that the affected employees are informed of and consulted before the transfer.

Pre-Writing Considerations of the Asset Purchase Agreement

There are six crucial elements that you need to consider in the pre-writing stage of your agreement. Whether you are the buyer or seller, you need to include all these elements in your APA to protect the interests of both parties during every stage of the agreement:

Identify the entity

You must identify the parties entering the agreement. More often than not, corporate entities may have multiple independent subdivisions. For that reason, the correct identification of the parties involved in the agreement is fundamental.

Identification of assets being transacted

It may seem obvious to identify the assets being purchased, but you must be as detailed as possible in this part. Detailed descriptions of specific assets should be given. For instance, you could indicate the available space for construction and parking, acreage, and building of its lands. The most significant difference with the asset purchase is that the buyer will only obtain ownership of the asset with no liabilities.

Indicate the payment terms

Price is a vital part of the asset purchase agreement, as are the terms of how the payment will be made. For instance, if a transaction involves seller financing, the buyer may remit a portion of the price and then sign a promissory note for the purchase price balance.

The debts also fall under the price negotiations. That means if an asset is involved with loans, both parties involved need to agree on who takes responsibility for it. This section also indicates if the buyer should deliver the payment all at once or in installments.

Representation and warranties

There are certain things that both parties rely on as part of the transaction. That includes the representations and warranties section, which covers such things as the fitness of the assets for specific purposes as well as the condition of sold items. In this section, the agreement could also indicate the legal status of the parties entering the contract.

The warranty, in this case, acts as an indemnity in a case where the asset fails to meet the agreed-upon conditions. Mostly, it favors the buyer, as the seller is required to provide the necessary warranties and disclaimers. Also, if the seller is not in a position to guarantee the condition and quality of the asset(s) being sold or purchased, they need to be warranted to shield the seller from extreme consequences like litigation or termination of the agreement.

Sealing agreement requirements

The conditions for closing the deal tend to vary depending on the nature of the transaction. The closing requirements include the approval of the sale by third parties involved, the delivery of the purchase price, and the need for the seller to make repairs or changes before the sale.

At this point, the involved parties can decide on their closing price adjustments. This section also needs to be as detailed as possible.

Boilerplate language

Boilerplate language may be standard across all contract types, but it can’t be ignored either. This section should highlight the state laws that govern the agreement and indicate that if any part of the agreement is deemed void, the rest of the contract remains valid. Also, it should highlight how amendments could be made to the agreement.

Enlisting the seller

After the sale, the seller may work for the buyer. If they receive any salary, it would be taxed as ordinary income. In fact, that should be clearly outlined in a separate consultant agreement or employment contract.

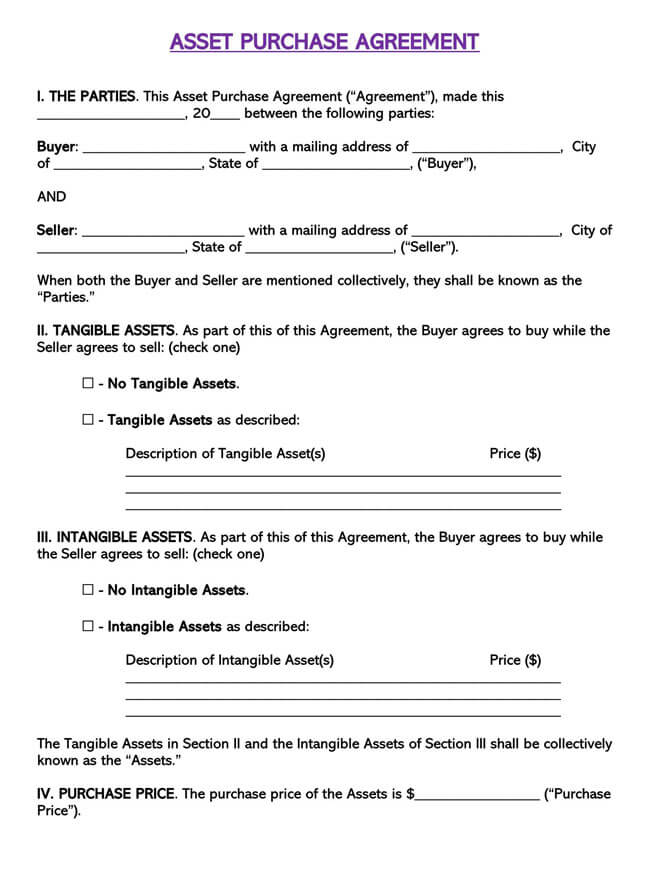

Writing an APA (Asset Purchase Agreement)

This section will help you draft the Asset Purchase Agreement correctly. This agreement will include the following clauses:

Date

Write down the details associated with the agreement, and the first statement of this agreement opens up by solidifying the agreement date. Date this agreement by adding the month, two-digit day, and two digits of the year. This is the date the contract is signed for execution or when the information is completed.

Record the buyer’s name

The next step is writing down the buyer in the agreement. That’s the party that will be required to submit a predetermined payment for the asset. More importantly, it would help if you recorded the purchaser’s name next to the term ‘Buyer,’ then the building number, street or road, and suite number, which will be found in the Mailing Address section.

Be sure that this section records the official names and addresses of the buyers. And if the purchaser is a business entity, make sure they register their legal names, including LLC, Corp, or Corporation.

Mention seller in the paperwork

The owner of the asset in this agreement should take the ‘Seller’ section. That said, locate the first section of the seller, then go ahead and fill in the relevant details. That includes the full name of the seller, including the mailing address. A reminder of the seller’s mailing address will also be expected again in the term ‘City of.’

Record sales for tangible assets

Before even defining the specifics of this sale, the asset in question should be defined. Therefore, in this agreement, both parties should agree if the item is tangible or not. It would help if you then marked the appropriate section. If the buyer is purchasing intangible assets but not any physical objects, this agreement document should also be indicated. Also, the price of the investment should be named in this section for clarification by both parties.

Reporting of intangible assets

The third part seeks to define the sale of intangible property. And if the property being purchased is intangible, then ensure it’s highlighted in the contract.

Requested purchase price

The actual payment that the buyer should pay the seller to complete the transfer of the property for the purchaser to gain ownership must be recorded numerically. Keep in mind that this should be the total cost of the assets.

Deposit requirement

In most cases, the seller will require a deposit to initiate the sale. That’s usually the case, especially when the asset is expensive. In the section ‘Deposit,’ the box must be checked, and the deposit must be written down. But if a deposit is not required, you should write it down.

Asset inspection

Another crucial element of the agreement is the inspection. That said, the contract should include a clause stating whether the asset should be assessed or not.

Identify the provision of payment

The next step is listing down the method of payment for the asset and how the purchaser is planning to fulfill it. If the price is scheduled to be received at a predetermined date, then ensure you’ve written it down in the agreement.

But there’s a chance the buyer will not be required to pay in full and will use ‘Owner Financing.’ If that’s the case, write down a ‘payment option’ box and continue with this statement by giving a full detail of the payment process.

Financing status of the sale

How the payment is made should be discussed in full. In this section, you should include the time indicated if the payment process depends on the buyer’s financial capability to complete the purchase.

And suppose the purchaser will be paying for the concerned asset directly from his or her capital. In that case, that means the sale will not encounter any additional financing; then, you should mark the ‘Not Contingent’ statement in this section.

Third-party approval

A third-party approval may be a determining factor for the completion of this transaction. If that’s the case, you can check the box for ‘Approval by 3rd Party,’ and you also need to add the mailing address. But if the contract only depends on the Buyer and Seller, check the box labeled ‘No requirement.’

Closing date and cost

The agreement’s closing date and the cost must be listed in this section for confirmation and verification by both parties.

Reviewing the contract

In this section, both parties will sign off, showing that they’ve reviewed the agreement’s content and that it’s correct. Do not sign if any alteration is required.

The quality of the asset

There are unforeseen casualties that might happen before the closing date. As such, the value of the asset may depreciate during this period. In the agreement, the seller should list down the number of days they will require if such an occurrence happens, so they have the chance to renegotiate the deal.

Add arbitration and mediation terms just in case

Sometimes the deal doesn’t go as smoothly as it sounds. And that could result in unnecessary obstacles to the completion of this deal. In such cases, the parties involved will need an arbitrator to help solve the problem and eventually complete the sale. The mediating party should be listed in the deal, as should the state, to solve the dispute.

List the governing law

Each state has its own set of rules and regulations that will govern such a transaction. And with that in mind, you should list down the state in which the agreement was made and the laws governing it.

Once the agreement has been drafted, the seller should review the terms. Once the seller has agreed with the statements, it’s time to commit on paper, and that’s what they will have to do in this section. That will include the date and their official signature.

Commitment by the buyer

Lastly, the buyer will also have a chance to review the agreement. And once he or she agrees, they will also have to commit on paper. The buyer should include their official signature and the date.

Post-Completion Requirements

After the completion and signing of the agreement, there are some post-completion requirements the buyer would need to meet. That includes:

- The payment of stamp duty and land tax depends on the asset type before the transfer.

- VAT payment is chargeable on the transfer of most assets. That ensures you’ve taken all legal considerations into account during the asset transfer from the seller to the purchaser.

- Administrative matters like pensions, insurance, payroll, VAT, and PAYE

Capital Vs. Non-Capital Assets That are Transferred

Essentially, capital gains are the profit amounts a company makes on a capital asset. Capital gains can be further categorized into short-term and long-term gains, according to the IRS. The short-term gains are owned for a year or less and are taxed as ordinary income at 10%–37%.

On the other hand, long-term gains are usually owned for more than a year, and the tax brackets vary from one individual to the next. Long-term capital gains are broken down as follows:

- 0% for income less than $78,750

- 15% for income ranging from $78,750 to $434,550

- 20% for income greater than $434,550

Capital assets are significant property pieces such as precious metals, vehicles, household furnishings, stocks and bonds, real estate, jewelry, collectibles, art, and personal property.

Capital assets have a useful life that is usually longer than a year and are not intended for sale during business operations.

Non-capital assets are ones that don’t meet the criteria for capital assets and are regarded as controlled property.

These non-capital assets have a useful life of more than a year and come with an acquisition cost of precisely $1,000, but not more than $5,000 per unit. Non-capital assets could include real estate used by the business, inventory, intangible properties such as models, designs, trademarks, copyrights, patents, inventions, and barter agreement accounts.

Frequently Asked Questions

The best and most effective way is on paper, with third-party approval. Check out ‘How to Correctly Format an APA (Asset Purchase Agreement)’ above to see full details on formatting an APA.

After an asset sale, the company still exists. However, administratively, you will still need to take the necessary steps to dissolve it and deal with any remaining assets and liabilities.

Often, buyers prefer asset sales as they avoid inheriting the potential liabilities they would otherwise inherit through stock sales. Also, it protects buyers from potential disputes, such as product liability claims, contract claims, or employment-related lawsuits.

About This Article