Retirement planning involves preparing today for your future so that you continue meeting all your goals and dreams independently for the post-retired life. This usually entails setting your retirement goals, estimating your retirement budgets, and investing in growing your retirement savings. While each retirement plan is unique, based on an individual’s specific ideas on how they want to spend their retired life, using a retirement budget worksheet to plan your finances ensures that you do not run out of money in retirement and gives you peace of mind knowing that you will be able to maintain your day-to-day lifestyle without worrying about expenses.

This guide will discuss the importance of planning your finances using a retirement budget worksheet, how it works, how to categorize expenses in a worksheet, and the essential things needed to create a worksheet. We will also provide a comprehensive guide on creating a practical retirement budget worksheet and discuss how the worksheet can help you plan for your after-work life.

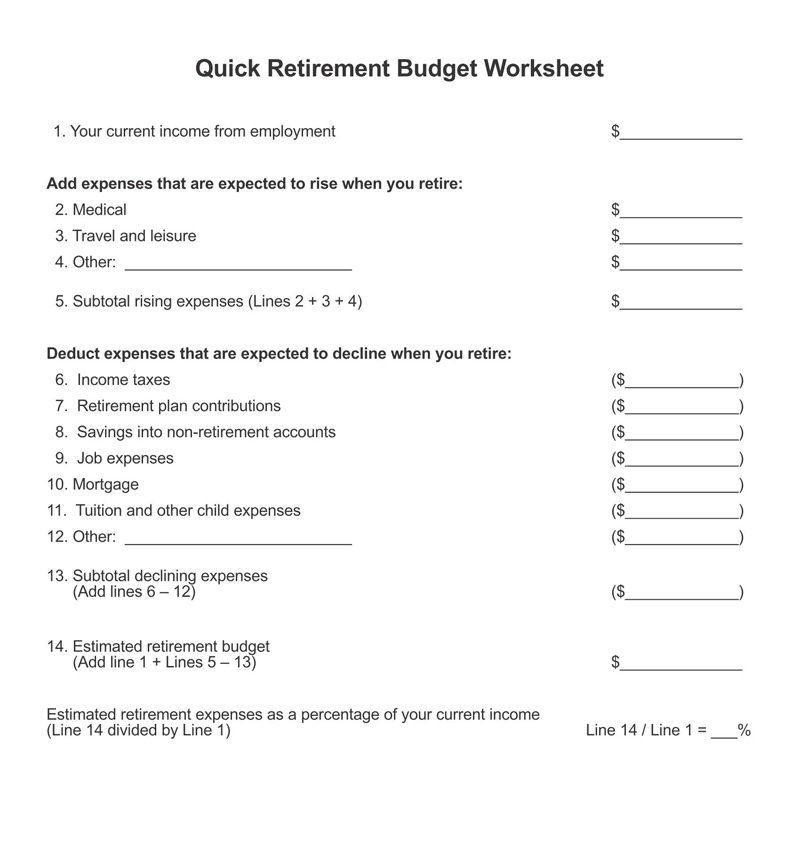

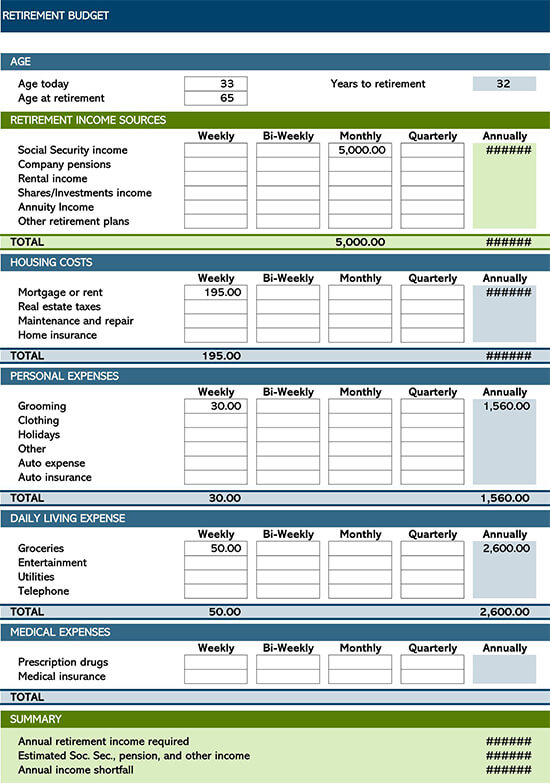

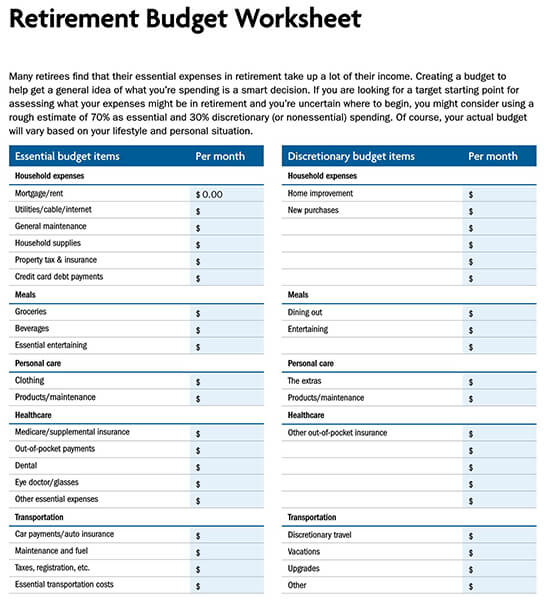

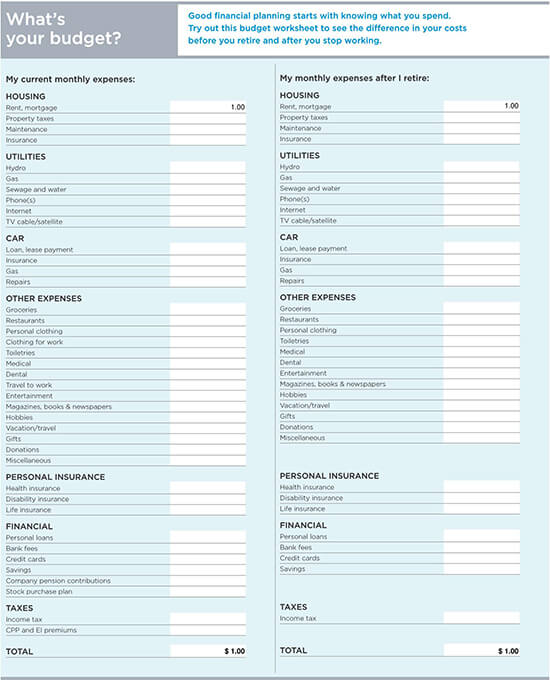

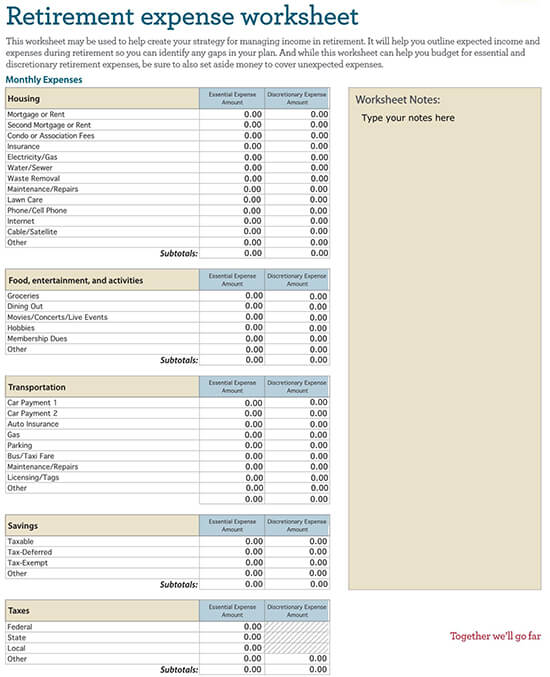

Retirement Budget Planner Templates

Importance of a Retirement Budget

Planning for your retirement means considering factors such as inflation, interest on savings, rents received on properties, part-time earnings, taxes, your retirement date, daily spending, social security, pensions, etc., all of which directly impact your retirement income.

A retirement budget is essential due to the following reasons:

Helps you to maintain your standards of living

While working, your day-to-day expenses and lifestyle are covered by your monthly income. However, there is no guarantee for a monthly income in retirement, and you want your current lifestyle to continue. However, you can plan a worksheet for your regular income to cover your daily expenses with a properly laid out budget.

Enables you to live within your means

Every retirement is a new lease in life. It is that point in life where you have all the time to explore new adventures, such as traveling to new places, picking up a new hobby, or starting a new venture. With all these in mind, it might be tempting to start overspending your sizable nest egg too soon, which can be financially dangerous. However, a reasonable budget enables you to control your spending with the help of a worksheet, making your savings last as long as possible.

Fight inflation

Inflation means the cost of all products and services is increasing on a daily or yearly basis. This usually affects the standards of living of most people. A solid retirement budget enables you to invest and grow your retirement funds, thus protecting them against inflation.

Prepares you for any unforeseen financial emergencies

After retirement, you would not want to be financially dependent on anyone in case of financial emergencies such as medical expenses or providing for your family and loved one’s needs. A good budget can help you build an emergency fund that will prepare you for unforeseen life circumstances.

Helps you leave a legacy

You have tirelessly worked hard to build a life of comfort and stability for your family. You want to ensure that this comfort lasts for decades in post-retirement and even in your absence. The proper budget enables you to build your retirement savings, enabling you to leave wealth behind for your family.

How Does a Retirement Budget Worksheet Work?

Generally, the worksheet helps you to determine whether your current savings rate is sufficient to support your living expenses in retirement or not. The worksheet gathers input, including your financial information and assumptions about factors affecting your retirement income. It makes use of financial formulas to project the value of your nest egg at retirement and gauge whether your retirement plan is on track. This is usually based on whether you will need the same or more or less than your current income.

The retirement budget worksheet is not an excellent predictor of whether you can retire but filling it in is a significant first step in planning your retirement. Customarily, the worksheet gives either of these two recommendations:

- If your expected retirement income covers your realistic expenses, you are on track for retirement, and you should stay the course with your current plans.

- If your expected retirement income does not cover your realistic expenses, you are not on track, and you need to save a specific amount of money for achieving your retirement goals.

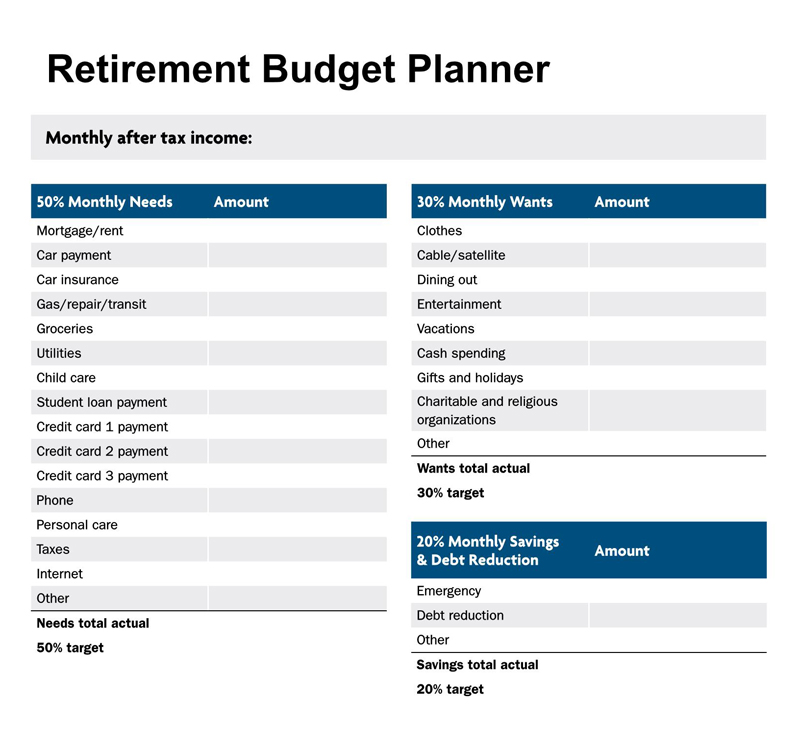

How to Categorize Expenses in Budget Worksheet

If you want to start planning for your retirement, you first need to recognize your financial needs and figure out what dollar amount you must save to achieve your retirement goals. Look for all your recurring monthly, quarterly, or annual payments and use highlighters to divide your expenses into the following categories.

Essential spending consists of regular monthly, quarterly, and annual expenses you will need to live everyday life. These include rent, mortgage payments, food, clothing, utilities, transportation, and healthcare.

Account for your healthcare costs

Typically, healthcare costs and health insurance costs are the main expenses you may face in your retirement. As such, it is prudent to assume that your healthcare costs will generally increase and outstrip inflation. In addition to medical costs, you should account for dental, vision, and hearing care as these usually become increasingly important as individuals age. Failing to consider the ever-increasing cost of health care can leave you without enough money to pay your other expenses, and this will render you financially dependable on other people, something you want to avoid by all means.

Non-essential monthly expenses

Non-essential monthly expenses include gym memberships, internet, cable tv, subscription services, and cell phone plans.

Required non-monthly expenses

Required non-monthly expenses include insurance premiums, property taxes, automobile registration, warranty extensions, etc. To calculate your monthly expense for the required non-monthly expenses, sum up these periodic expenses and divide the resulting figure by 12. Then, enter the resulting cost in your worksheet under the periodic expense category.

Discretionary spending

Factor in the extra things for which you want to have money. This includes all the fun stuff such as travel, hobbies, entertainment, outings by yourself or with your spouse and grandchildren. To find your monthly discretionary spending, consider how often or how much you want to spend on these fun retirement activities. You can then divide your discretionary income by 12, although your total spending may vary each month.

It is also significant to factor in how your hobbies and lifestyle may change, as this will likely affect the way you spend. For instance, if you want to spend your retirement life pursuing new and expensive hobbies, you will want to think about the trade-offs you will be willing to make to free up money for those activities. For example, you can consider living in a smaller home to reduce your monthly housing costs.

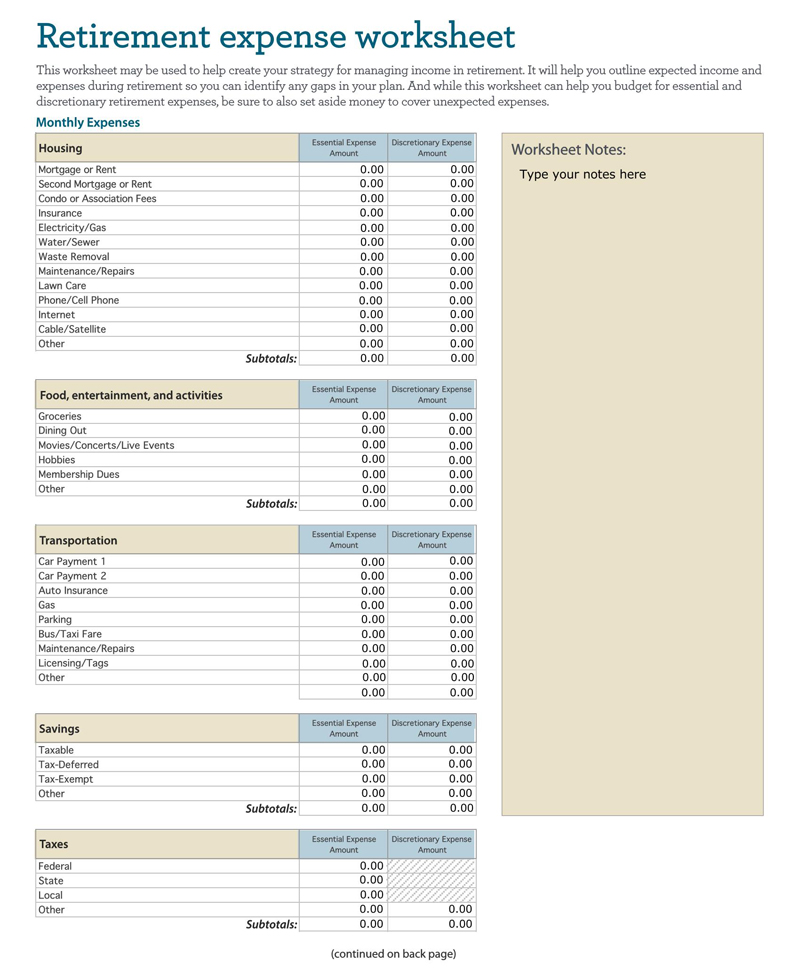

Data Required to Create a Retirement Budget Worksheet

To create an effective retirement plan using a retirement budget worksheet, you first need to gather some essential documents that will help you handle your income and spending. These include documents such as:

- Your recent bank account statements: A minimum of six months is considered sufficient, but it is wise to expand that to 12 months

- Your most recent credit card statement, at least six months or a maximum of 12 months

- If you, your spouse, or both are employed, you will need to have the last two pay stubs

- Your previous year’s tax return statements

- Highlighter pens help you identify and track spending and income categories, making it easier for you to enter them into your worksheet.

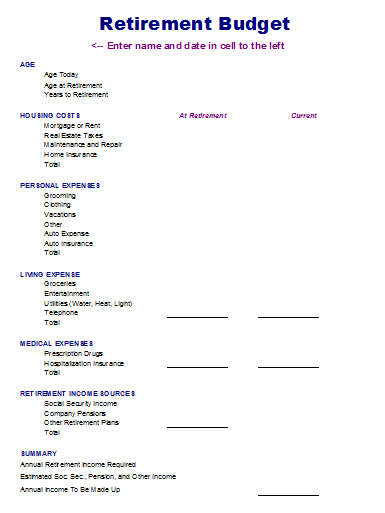

How to Make a Retirement Budget

The worksheets come in different forms and formats. Nonetheless, all retirement budget worksheets have one thing in common: estimating total retirement expenditure by working with estimates of spending in various, smaller budget categories.

Regardless of the worksheet model that you decide to use, the following is a detailed guide on how to fill your budget worksheet:

Estimate your retirement income

The first step of creating a retirement budget involves estimating how much retirement income you will need. In most cases, an estimate of about 70% to 80% is considered a reasonable budget in the worksheet, but this may vary depending on your annual spending. For example, if you are still working and your salary is approximately $100,000 per year, you can estimate your retirement income to be $70,000 to $80,000 annually as a starting point. You can further estimate what you will need monthly by dividing your annual income by 12 to determine your monthly budget.

List your expected spending/expenses

The next step of creating your worksheet involves listing your expected expenses. This includes essential expenses, non-essential monthly expenses, discretionary spending, and required non-monthly expenses. For most retirees, these expected expenses remain the same. However, costs associated with healthcare and Medicare may change from time to time.

Determine the expenses that will change in retirement

Upon retirement, you will probably need to reassess your financial situation to determine the expenses you may have had before retirement that won’t be necessary for your new stage of life and those you previously didn’t have. Still, you have to pay for it in retirement. In addition, your expenses will often change according to the stage of retirement you are in; therefore, you should review your budget annually to make provisions for factors such as inflation and a decrease or increase in certain expenses.

Common examples of expenses that will change in retirement include:

- Travel expenses: most retirees tend to travel more in their early retirement years

- Medical expenses: these increases in your later retirement years

- Life insurance premiums: you are more likely to pay less life insurance premiums at a later stage of your retirement

- Debts, mortgages, or car loans to service: These expenses decrease for most retirees

Include the significant lifestyle changes

Next, factor in the lifestyle changes that you will need to make in your retirement. For instance, if you wish to relocate to a new area with a higher cost of living or venture more into new expensive hobbies such as traveling the world, you might need to adjust your budget accordingly. Keep in mind that every retiree’s needs and desires are unique, and you need to focus on choices that will bring you a feeling of fulfillment and purpose during your post-work life.

How much money is coming in

The fifth step of creating your worksheet involves calculating how much money you will be getting each month. In retirement, monthly income may come in from various sources rather than a single paycheck from your employer each month. For example, if you or your spouse have enough work credits, income can come from Social Security and pensions. Money can also flow in from investment accounts such as 401(k) accounts, IRAs, income from rental investments, part-time jobs, etc.

Outline a spending plan

After you have estimated your fixed expenses, adjusted your budget for your new lifestyle changes, and factored in your realistic income streams, it is time to outline your spending plan. You can use a budgeting tool or system that allows you to track your expenses. The most appropriate budgeting tools to choose from include an app or software, a worksheet, a spreadsheet, or pen and paper.

Regardless of the type of budgeting tool you decide to use, here is how to outline your spending plan:

- Step 1- Add up what you expect your actual household income to be in retirement

- Step2- include your Social Security benefits, retirement account withdrawals, part-time job income, 401(k) accounts, IRA, rental income, and other income sources.

- Step 3- Compare the resulting figure to your estimated retirement expenses.

- Step 4- Subtract the total expense from your overall income.

Note

To ensure safety, your monthly income must completely cover your expenses and leave you money to do the things you love to do. However, if the difference is a negative number or does not help you achieve your financial goals, you must find a way to cut your expenses or increase your income.

Test drive your budget

Once you have set up your budget, it is wise to test drive your budget before you retire. Set the budget as your new monthly budget while you are still working. Consider directing any income that exceeds your new monthly budget to retirement investment accounts such as the 401(k) account, IRA, or invest it in other retirement plans to boost your future retirement income.

If you happen to spend more than expected, go back to the drawing board, and determine any adjustments that can be made. Test-driving your retirement budget several months before you retire gives you a clear indication of what you need to live on in your retirement. Then, you can make necessary plans to boost your savings while still working to have more income available later. You can also lower your fixed expenses to ensure that you live within your means.

How is a Retirement Budget Worksheet Helpful?

A retirement budget worksheet is a form that can be downloaded through online means and can be customized to suit a user’s unique budget needs. The worksheets offer a great way of tracking your retirement finances, helps you predict your income and expenses, and ensure that you are ready for retirement. The budgeting worksheet is usually easier to use than a budgeting spreadsheet. It offers you a solid overview of your finances, and it is usually the first recommended step in creating an effective budget plan.

Frequently Asked Questions

To calculate your fixed costs and flexible costs, sum up all your fixed expenses, then total all your other non-fixed expenses separately and divide your fixed expenses into your total expenses.

Once you have created your budget, it is essential to try it out practically several months before retiring. Then, you can set it as your new monthly budget to determine whether it is realistic or not. Of course, if you spend more than anticipated, you should make the necessary adjustments, such as compromise in other areas, saving more, or taking up side jobs to bring in extra income, etc. However, if you are financially comfortable after test driving your budget, you know your budget is on track and you are ready to retire.

About This Article